Generational wealth starts with one brave family member who dares to do something no one else has done.

If you come from a humble family like mine, no one likely taught you about generational wealth and money, as they may not have understood it themselves.

This is why I created this blog to explain everything I am doing to generate wealth for myself and my future generation.

So what is generational wealth? Let us start there.

What Generational Wealth Really Means (And What It Doesn’t)

At its core, generational wealth is the accumulation of valuable assets, such as financial, real estate, business, and intellectual property, that are preserved and passed down from one generation to the next.

Its primary purpose is to provide a foundation of financial security, stability, and increased opportunity for future descendants.

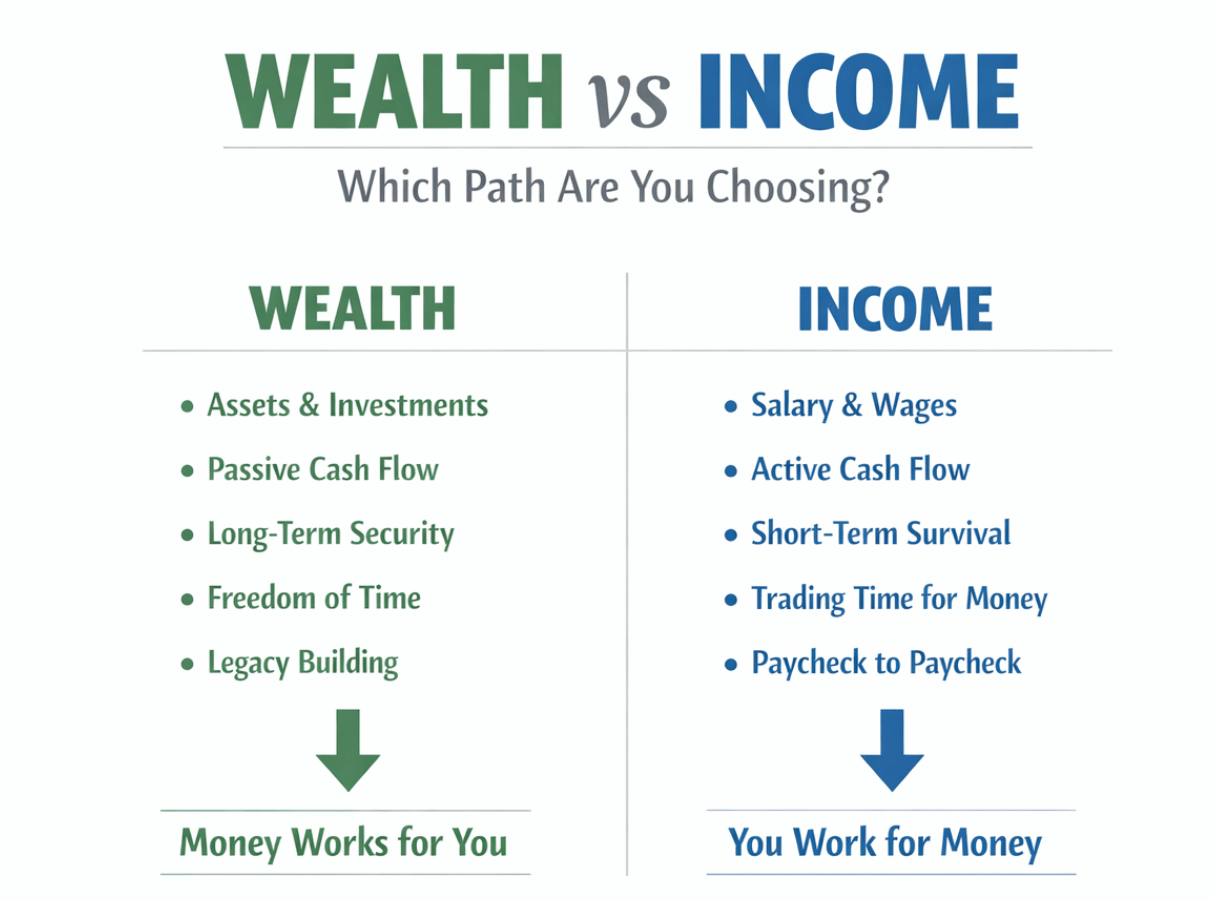

The critical distinction here is between assets and income.

Income is the money you earn from your job or business. Income is considered active and temporary because it ceases when you stop working.

Assets are things you own that hold or increase in value over time and generate income for you. They are passive, enduring, and they work while you sleep.

As the renowned financial educator Robert Kiyosaki frames it in Rich Dad Poor Dad, “The rich focus on their asset columns while everyone else focuses on their income statements.” Generational wealth is built by systematically converting income into lasting assets.

Common Myths Debunked

Let’s dismantle the greatest barriers to understanding.

Myth 1: “It’s only for the ultra-rich.”

This is the most pervasive and damaging myth. While the scale differs, the principles are universal. A family that leaves a paid-off home, a funded education account, and a solid investment portfolio to their children has built generational wealth. It’s about mindset and strategy at any level, not just about owning a private island.

Myth 2: “It guarantees lazy, entitled heirs.”

Poor planning and a lack of communication can lead to this outcome, but it is not inevitable. Intentional wealth building includes instilling financial literacy, values, and a sense of stewardship in the next generation. The goal is to provide opportunity, not a life of idleness.

Myth 3: “It’s all about luck or a massive inheritance.”

While receiving an inheritance can accelerate the process, most enduring family wealth is built deliberately over decades.

It results from consistent investing, debt avoidance, smart financial decisions, and educated risk-taking, not a lucky lottery ticket.

The Powerful Impact: Opportunity, Security, and Choice

Why is this pursuit so powerful? The benefits extend far beyond a bank balance.

Opportunity

It can fund higher education without crippling debt, provide seed capital for a family business, or enable a career change based on passion rather than pure necessity.

Security

It creates a financial safety net that can help a family cope with job loss, medical crises, or economic downturns without falling into poverty.

Choice

Perhaps most importantly, it grants time and freedom. It can reduce the relentless pressure of living paycheck-to-paycheck, allowing future generations to make life choices aligned with their values, not just their immediate financial needs.

What Constitutes Generational Assets?

Generational wealth is a diversified portfolio of tangible and intangible pillars, not a single entity. Understanding these components is the first step to building them.

The 5 Key Pillars of Generational Wealth

Financial Assets & Investments

This is the most liquid and common pillar. It includes:

Public Market Investments

Stocks, bonds, mutual funds, and ETFs. These offer growth and, in some cases, dividend income.

Retirement Accounts

401(k)s, IRAs (Traditional and Roth). These are not just for retirement spending; they can be powerful, tax-advantaged vessels for wealth transfer to heirs.

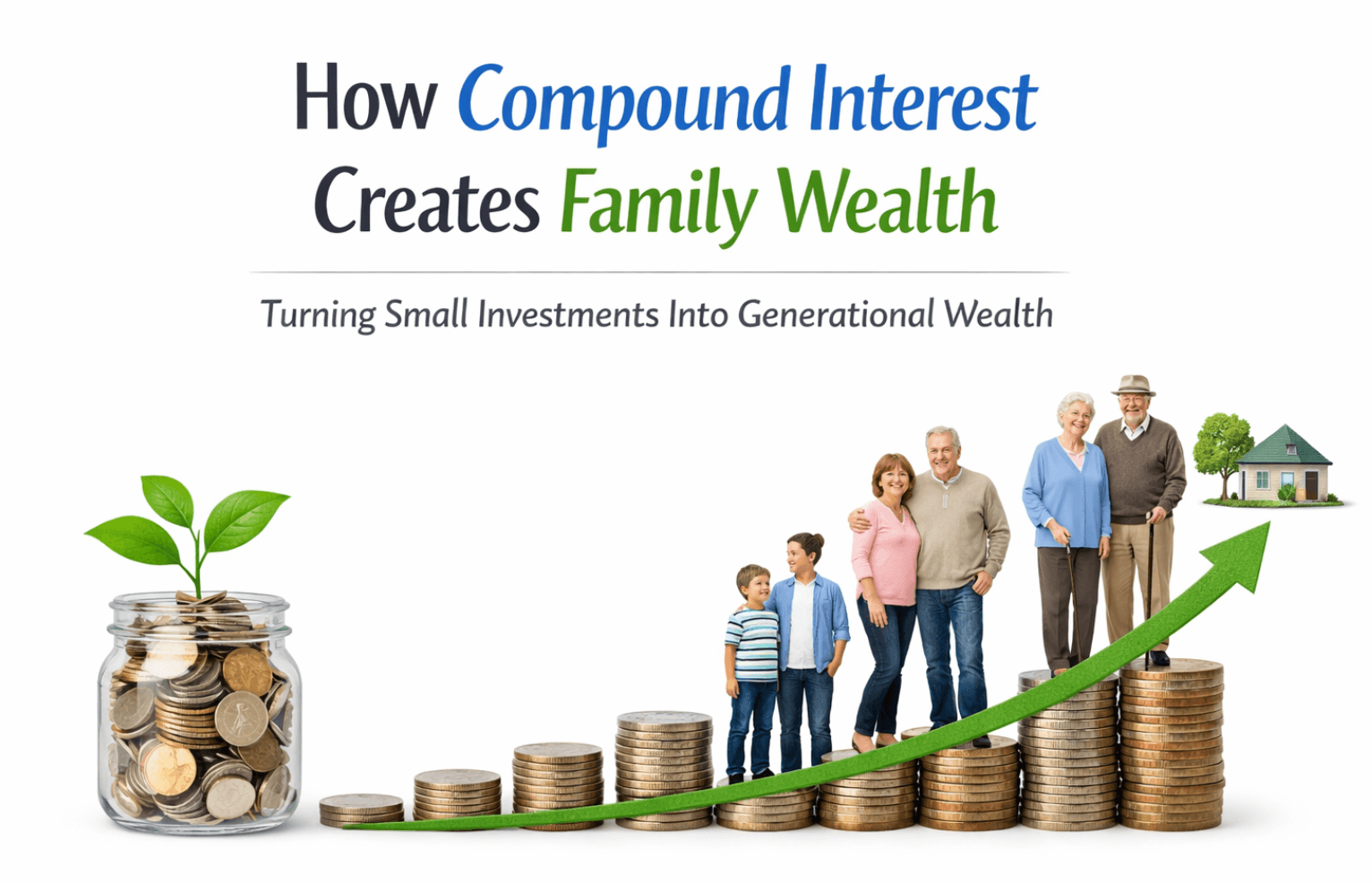

The Magic of Compound Interest

This is the non-negotiable engine of this pillar. Albert Einstein allegedly called it the “eighth wonder of the world.”

It’s the process where your investment earnings generate their own earnings over time. Starting early is your greatest advantage.

Example: Investing $300 a month starting at age 25 with a 7% annual return yields over $675,000 by age 65. Starting at age 35 yields about $305,000. The ten-year head start is worth nearly $370,000 more.

Real Estate & Land

A classic, tangible form of wealth that often appreciates and generates income.

Primary Residence

Building equity in a home is a forced savings plan and a future asset that can be passed down, lived in, or sold.

Rental Properties

These provide ongoing passive income and benefit from property value appreciation.

Land

As Mark Twain said, “Buy land, they’re not making it anymore.” It’s a finite asset that historically holds value.

Business Ownership & Intellectual Property

This is the wealth accelerator.

Family Business

A profitable, well-structured business can be a multi-generational source of income, employment, and family identity.

Intellectual Property (IP)

Patents, copyrights, trademarks, and royalties. This is the pinnacle of “assets that work for you.” Even after the creator’s death, a book, song, invention, or software code can continue to generate income for decades.

Life Insurance & Trusts

These are the transfer and protection mechanisms, not necessarily growth drivers.

Permanent Life Insurance

Policies like whole life can provide a tax-free death benefit to heirs, offering immediate liquidity to pay expenses or debts.

Trusts

Legal entities that hold assets for the benefit of specific people. They avoid the public, often lengthy probate process and allow you to set precise terms for how and when heirs receive assets (e.g., “25% at age 25, 50% at 30, the remainder at 35”).

Human & Intellectual Capital

This is the most critical, yet most overlooked, pillar. It is the knowledge, values, and skills passed down.

Financial Education

Teaching children about budgeting, investing, and debt. This will equip them to carry on your legacy after your departure.

Work Ethic & Values

Instilling the principles of hard work, delayed gratification, and philanthropy. Teach them the value of working hard, providing value, and multiplying assets.

Family Legacy & Social Capital

The reputation, relationships, and “know-how” a family accumulates.

Without this pillar, the other four are at extreme risk. “Shirtsleeves to shirtsleeves in three generations” exists because the first generation builds the wealth, the second grows up with it but may not understand the work behind it, and the third, raised in comfort, squanders it. Human capital breaks this cycle.

How to Start Building Generational Wealth from Scratch?

I come from a deprived family in Tanzania. I have built everything I am. I will be honest with you: it is difficult and lonely, and most people, especially childhood friends and family members, may not understand your experiences.

Feeling overwhelmed is normal. Break it down into this actionable, step-by-step blueprint.

Mindset Shift: From Consumer to Builder & Investor

I believe that everything starts by changing the way you think, change the way you think, and you will change your life.

Your first task is to change your relationship with money. Instead of viewing income purely for lifestyle consumption, begin to see a portion of it as “seed capital” for your future asset portfolio. Prioritize acquiring assets that appreciate or generate income over buying liabilities that depreciate.

Step 1: Fortify Your Foundation

You cannot build a sturdy skyscraper on quicksand.

Build an Emergency Fund (3-6 months of expenses)

This cash buffer prevents you from going into high-interest debt when unexpected costs arise. It safeguards your emerging assets from liquidation during a crisis.

Aggressively Eliminate High-Interest Debt

Credit card and personal loan debt can drain your wealth. The interest you pay is money actively working against your wealth-building goals. Tackle your debts before aggressive investing.

Step 2: Consistent Investing

This is where compound interest starts working in your favor.

Automate Everything

Set up automatic monthly transfers from your checking account to investment accounts. This makes building wealth a passive, non-negotiable habit.

Start with Retirement Accounts

Maximize employer 401(k) matches (it’s free money), then contribute to a Roth IRA for its tax-free growth and withdrawals in retirement.

Embrace Low-Cost Index Funds

For beginners, these are ideal. They provide instant diversification across hundreds of companies and have very low fees (expense ratios). A simple S&P 500 index fund is a perfect core holding.

The “Set It and Forget It” Philosophy

Time in the market beats timing the market. Consistency over decades is infinitely more important than picking hot stocks.

Step 3: Strategic Homeownership

For most families, their home is their largest single asset. While not suitable for everyone at every life stage, building equity through mortgage payments is a powerful form of forced savings and a cornerstone of net worth.

Step 4: Invest in Yourself

Your greatest income-generating asset is you.

- Continuously upgrade your skills and education to increase your earning potential.

- Consider starting a side business. What begins as a side hustle can evolve into a scalable asset and the seed of a future family enterprise.

The Art of Wealth Transfer & Protection

Building wealth is only half the battle. Without a plan for its transfer, your legacy can be eroded by taxes, legal fees, and family conflict.

Why a Will is Your Non-Negotiable First Step

If you die without a will (intestate), the state decides how your assets are distributed based on a generic formula.

This process (probate) is public, slow, expensive, and may not reflect your wishes. A legally valid will is the absolute bare minimum.

Introduction to Key Transfer Tools

Trusts

Think of trust as a specially labeled box for your assets. You set the rules for the box. A Revocable Living Trust allows you to control the assets during your life and smoothly transfer them to beneficiaries after death, avoiding probate. More complex Irrevocable Trusts can help with estate tax minimization.

Beneficiary Designations

Often overlooked! These are the forms you fill out for life insurance policies, retirement accounts (IRAs, 401(k)s), and certain bank accounts. They bypass your will and probate entirely and go directly to the named person. Review them regularly!

Gifting Strategies

You can gift up to the annual exclusion amount ($18,000 per recipient in 2024) to any number of people tax-free each year. This is a simple way to reduce your taxable estate while helping heirs during your lifetime.

The Crucial Role of Professional Guidance

Do not DIY your estate plan with online forms. Assemble your legacy team:

Estate Planning Attorney

Drafts legally sound wills, trusts, and powers of attorney.

Fee-Only Financial Planner

Provides unbiased advice on growing and structuring your assets for transfer.

CPA

It advises you on tax implications during your life and for your heirs.

View their fees not as an expense, but as an investment in legacy infrastructure that can save your family tens or hundreds of thousands of dollars.

Values, Communication, and Literacy

The “soft” elements determine whether wealth survives or is destroyed within a generation.

Family Governance & Communication

Silence about money breeds misunderstanding and entitlement.

- Have age-appropriate, open conversations about finances, values, and responsibility.

- Discuss the family’s financial philosophy: Is it about creating opportunity? Supporting education? Encouraging entrepreneurship?

- As children mature, involve them in certain discussions to prepare them as stewards.

Teaching Financial Literacy to the Next Generation

This is your responsibility.

Young Children

Use allowances to teach saving, spending, and giving.

Teenagers

Introduce budgeting, basic investing, and the true cost of debt (e.g., car loans).

Young Adults

Discuss topics like retirement account benefits, credit scores, and the details of your estate plan.

Your Legacy is More Than Money

Wealth is a tool. Define what it should build.

Philanthropy

Establishing a family giving tradition creates unity and purpose.

Ethical Will

Write a letter sharing your life lessons, hopes, and values for your descendants.

Family Narratives

Share stories of struggle and perseverance that built the wealth, not just the results.

FAQ: What is Generational Wealth?

Can I build generational wealth if I have a normal income?

Absolutely. It’s not how much you earn, but how much you save and invest over time. A moderate income with a high savings rate will outperform a high income with a spending problem every time.

How much money do I need to start?

You can start with what you have. Many brokerages allow you to buy fractional shares of stocks or ETFs. Setting up an automatic transfer of $50 or $100 a month into a low-cost index fund is a powerful, achievable start that harnesses compound growth.

What’s the biggest mistake people make?

The biggest mistake people make is neglecting the twin pillars of estate planning and their preparation. Failing to have a legal transfer plan and failing to teach the next generation about financial stewardship is a recipe for the “three-generation cycle” of loss.

When should I start estate planning?

Now. Estate planning is about having a plan for your assets and minor children if something happens to you. It is not a function of how much you own. Every adult with any assets or dependents needs basic documents.

Conclusion: Your Legacy Journey Begins Today

Generational wealth is not a secret held by the fortunate few. It is the natural result of a careful approach: regularly turning your earnings into a variety of assets, secured by strong legal protections, and supported by common values and knowledge about money.

It is a marathon, not a sprint, built one smart decision at a time. The single most important step is to begin.

The choice you make today, to open an investment account, to increase your 401(k) contribution by 1%, to schedule a consultation with a financial planner, or to have a money conversation with your child, is the seed you plant for your family’s future forest.

Your legacy isn’t written by where you start, but by the direction you choose to go. Start building that direction today.

Ready to take the next step?

Primary Action

Schedule a 30-minute consultation with a fee-only financial planner to discuss your specific goals and create a personalized starter plan.

Secondary Action: Download my personal wealth operating system.

Let’s Connect

What’s the one financial lesson or value you most want to pass on to the next generation? Share your thoughts in the comments below; let’s learn from each other’s visions for a lasting legacy.

{kind=link}