Most people talk about wealth as if it’s something you get.

I see it differently.

Real wealth is something you build slowly and intentionally, and with people you may never meet in mind.

Generational wealth isn’t about flashy success or overnight wins. It involves establishing assets, systems, and values that persist long after your departure. It’s quiet. It’s disciplined. And it requires thinking far beyond your next paycheck.

In this guide, I’ll walk you through exactly how to build generational wealth, not from theory, but from a long-term, real-world perspective. No shortcuts. No hype. The concepts are based on principles that have been developed over decades.

What Is Generational Wealth?

Generational wealth is often misunderstood. Many people think it simply means leaving money behind for their children. That’s only a small part of it.

True generational wealth is the combination of assets, systems, and financial education passed from one generation to the next. It’s not just what you leave; it’s what lasts.

Money without structure disappears. Assets without education get sold. Wealth without values erodes.

Generational wealth is designed to survive time, mistakes, and market cycles.

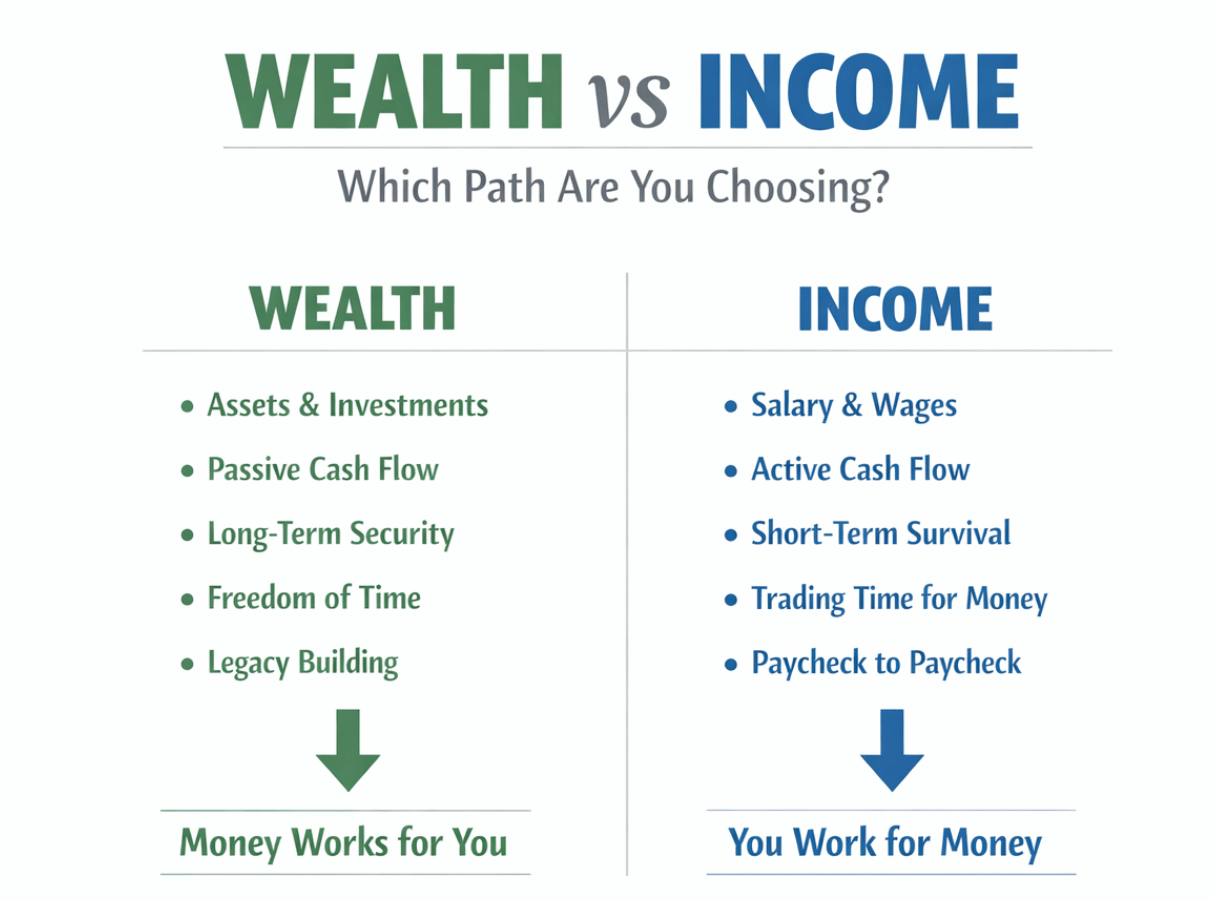

Generational Wealth vs. Personal Wealth

Personal wealth focuses on you: your lifestyle, your income, and your comfort.

Generational wealth focuses on continuity.

Personal wealth asks, “How much can I earn?”

Generational wealth asks, “How long can this last?”

One is consumption-based. The other is ownership-based.

That difference alone explains why so much wealth vanishes within a generation or two.

Why Most Wealth Disappears by the Third Generation

There’s a saying that wealth is built in one generation, preserved in the second, and lost in the third. That doesn’t happen because money is inherently flawed; it happens because systems and education are lacking.

Without financial literacy, heirs often lack an understanding of how the wealth was accumulated.

Without structure, assets are mismanaged.

Without values, money becomes entitlement instead of responsibility.

Generational wealth doesn’t fail because of bad luck. It fails because of inadequate preparation.

The Generational Wealth Mindset (This Comes First)

Before you talk about investing, businesses, or assets, you need the right mindset. Without it, everything else collapses.

Thinking in Decades, Not Paychecks

Generational wealth requires long-term thinking. Not five years. Not ten. Think in decades.

Most people optimize for speed. I optimize for durability.

Quick money feels good, but it rarely lasts. Slow money compounds quietly, and that’s where real power comes from.

When you start asking, “Will this decision still make sense in 20 years?” your behavior changes.

Delayed Gratification in a Short-Term World

We live in a culture that rewards immediacy. Spend now. Upgrade now. Flex now.

Delayed gratification is uncomfortable, but it’s also a superpower.

Every dollar you don’t spend today is a worker you can deploy tomorrow. Delaying any lifestyle upgrade allows compounding to work more effectively over time.

Discipline isn’t restriction. Its direction.

Breaking the Earn–Spend–Repeat Cycle

Most people never escape this loop. People earn money, spend it, and then repeat this cycle indefinitely.

To build generational wealth, you must move from consumer to owner.

That shift starts when you treat surplus income as capital, not entertainment.

Step 1 – Build a Strong Financial Foundation

No legacy is built on chaos.

Before you invest or expand, your financial base must be stable.

Master Cash Flow Before Investing

It doesn’t matter how much you earn if you don’t control where it goes.

Cash flow management is the foundation of wealth. You need to know:

- What comes in

- What goes out

- What remains available to build with

I’ve seen high earners stay broke because they never mastered this step.

Eliminate High-Interest Debt Strategically

Not all debt is equal. High-interest consumer debt is toxic to compounding.

Debt with interest rates that outpace conservative investment returns slows everything down. Eliminating it doesn’t just reduce stress. It increases future options.

Create an Emergency Buffer

Emergencies are one of the biggest reasons long-term plans fail.

A proper emergency fund isn’t about fear. It’s about continuity. It prevents you from selling assets or abandoning strategy when life happens.

Step 2 – Increase Income With Purpose

Income is not wealth, but it’s the engine that builds it.

Active Income as the Fuel

Your skills, knowledge, and effort are your first assets.

The goal isn’t to work forever. It’s to use active income to acquire assets that don’t require constant labor.

Build Multiple Income Streams Over Time

Diversification isn’t just for investments. It applies to income, too.

Multiple income streams reduce risk and increase resilience. The key is to build them intentionally, not chaotically.

Avoid Income Traps

Busy doesn’t mean wealthy.

Many people chase income without ownership. If your income stops the moment you stop working, you’re still exposed.

Ownership is the bridge between income and generational wealth.

Step 3 – Invest in Assets That Outlive You

This is where generational wealth truly begins.

Why Assets Matter More Than Income

Income is temporary. Assets are persistent.

Assets generate cash flow, appreciation, or both, without requiring constant input. That’s how wealth continues when you’re no longer working.

Core Asset Classes for Generational Wealth

While strategies vary, most generational wealth is built through:

- Equities (stocks and index funds)

- Real estate

- Businesses and equity ownership

Each has strengths, risks, and timelines. The goal isn’t perfection; it’s consistency.

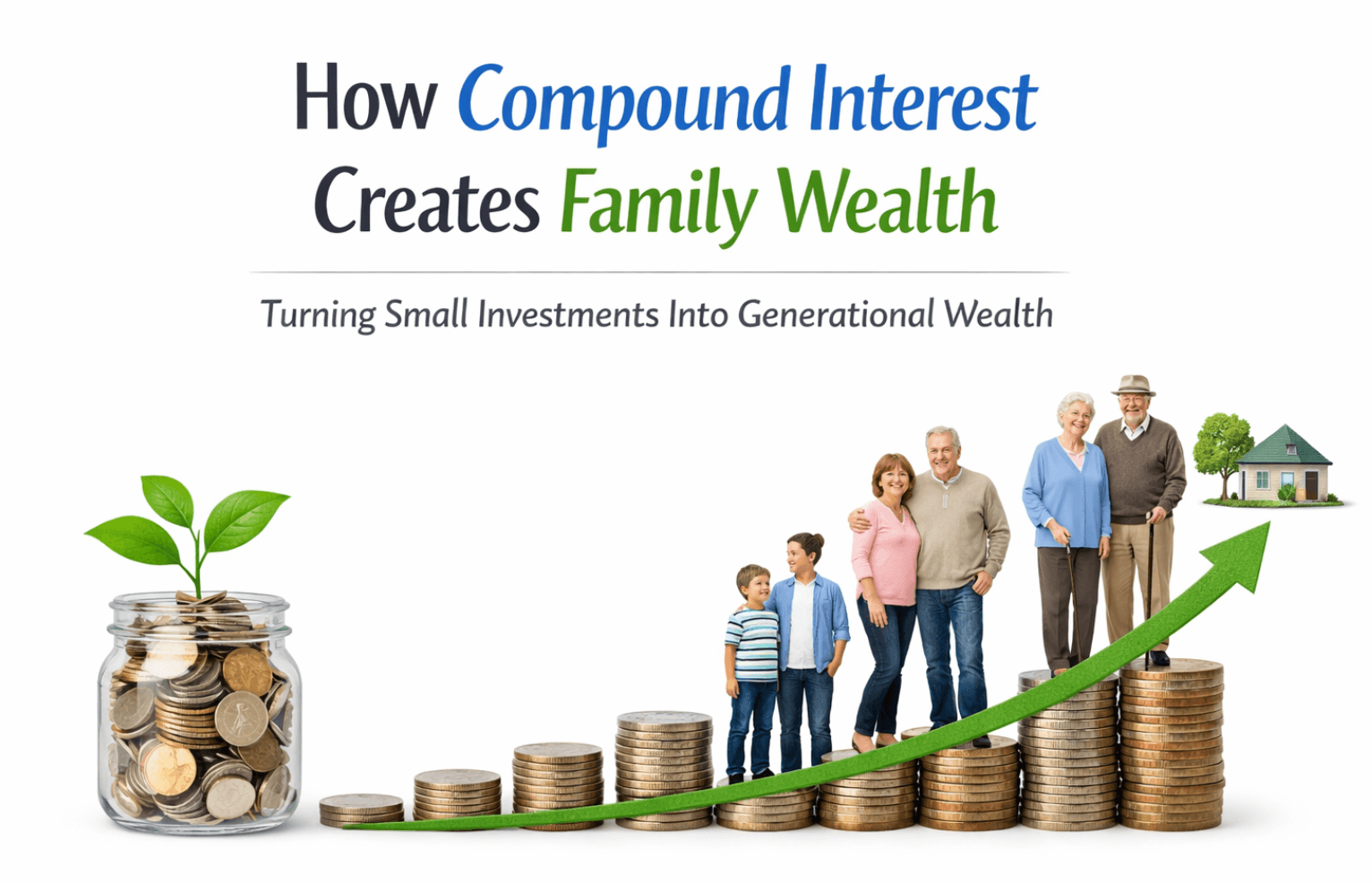

The Power of Compounding

Compounding doesn’t impress people early. That’s why most ignore it.

But over 20–40 years, it becomes unstoppable.

Investing for a long period is more beneficial than trying to predict market timing. Always.

Step 4 – Protect What You Build

Building wealth without protection is like filling a bucket with holes.

Why Protection Is Part of Wealth Building

One lawsuit, illness, or unexpected event can undo decades of effort.

Protection isn’t pessimism; it’s responsibility.

Insurance as a Preservation Tool

Life insurance, health coverage, and asset protection exist to preserve momentum.

They keep long-term plans intact when short-term crises appear.

Legal Structures Matter

Wills, estate planning, and proper ownership structures ensure that assets transfer intentionally, not accidentally.

This is where legacy becomes concrete.

Step 5 – Teach Financial Literacy Across Generations

Money without education is temporary.

Why Education Is the Missing Link

Most families pass down money without context. That’s a recipe for loss.

Financial education explains:

- How wealth was built

- Why certain decisions were made

- How to preserve and grow assets

Teaching Children About Money Early

Children learn more from behavior than from lectures.

When they see long-term thinking modeled daily, it becomes normal, not restrictive.

Passing Down Values, Not Just Assets

Generational wealth is as much about character as capital.

Responsibility, patience, and stewardship must be taught intentionally.

Step 6 – Build Systems, Not Just Wealth

Systems make wealth repeatable.

Automate What You Can

Automated saving and investing reduce emotion and inconsistency.

Wealth grows faster when decisions don’t rely on motivation.

Document Your Financial Philosophy

Clear documentation prevents confusion and conflict later.

Your financial principles should be written, not assumed.

Plan for Continuity

Eventually, you won’t be there.

Generational wealth planning answers the question, “What happens next?”

Common Mistakes That Destroy Generational Wealth

- Chasing shortcuts

- Ignoring taxes and long-term costs

- Failing to communicate with family

- Treating money as status instead of responsibility

Wealth doesn’t disappear suddenly. It erodes quietly through neglect.

Can You Build Generational Wealth Starting From Zero?

Absolutely.

Starting point matters far less than direction and consistency.

I’ve seen people with high incomes sabotage themselves, and others with modest beginnings build extraordinary legacies.

Time rewards discipline, not privilege.

Realistic Timelines

Generational wealth typically takes more than a decade to build. Think in:

- 5-year foundations

- 10-year asset accumulation

- 20+ year compounding phases

Progress may feel slow, but it’s cumulative.

My Personal Philosophy on Generational Wealth

I don’t believe wealth is about ego.

I believe it’s about responsibility.

My current endeavors aim to alleviate future struggles, not only for my family but also for future generations who may not even recognize my existence.

That is the long-term strategy I am pursuing.

FAQ: How to Build Generational Wealth

What is the fastest way to build generational wealth?

Building lasting generational wealth takes time. In my experience, the most reliable path is increasing income intentionally, investing consistently in long-term assets, and allowing compounding to work over decades. While shortcuts may generate money, they seldom lead to the creation of a lasting legacy.

How long does it take to build generational wealth?

Generational wealth is typically built over 20 to 40 years. While you may see progress within the first decade, true legacy wealth requires time, consistency, and discipline. The goal isn’t speed. Its durability.

Do you need to be rich to create generational wealth?

No. You don’t need a high income to start building generational wealth—you need the right habits. Many families with modest incomes have built lasting wealth by controlling cash flow, investing early, and avoiding lifestyle inflation. Direction matters more than the starting point.

What assets are best for generational wealth?

The strongest assets for generational wealth are those that produce income, appreciate over time, or both. These typically include diversified stock investments, real estate, and business ownership. The key isn’t chasing returns but owning assets that can compound and be passed down responsibly.

How can we prevent the loss of generational wealth?

Protection starts with structure and education. Legal planning, insurance, and clear documentation help preserve assets, but teaching financial literacy across generations is just as important. Wealth lasts when heirs understand both the assets and the responsibility that comes with them.

Can generational wealth be built in one generation?

Yes, but it requires intentional sacrifice. One generation can lay the foundation by building assets, documenting systems, and educating the next. Even if full compounding takes longer, the first generation sets everything in motion.

What role does financial education play in generational wealth?

Financial education is the glue that holds generational wealth together. Without it, assets are often misused or sold.

When families pass down knowledge alongside money, wealth becomes sustainable instead of temporary.

Is generational wealth only about money?

No. Money is just one component. Generational wealth also includes values, discipline, decision-making frameworks, and long-term thinking. These are often more powerful than money itself.

How can parents teach children about generational wealth?

The most effective way is by example. Children learn from what they see—how money is saved, invested, and discussed. Simple lessons about ownership, patience, and responsibility, taught early, shape how wealth is handled later in life.

What is the biggest mistake people make when trying to build generational wealth?

The biggest mistake is chasing speed instead of sustainability. When people prioritize immediate money over long-term systems, wealth becomes fragile. Generational wealth is built slowly, protected intentionally, and passed down deliberately.

Final Thoughts: Generational Wealth Is Built Quietly

Most people chasing wealth want attention.

Most people building a legacy don’t need it.

Generational wealth grows through boring consistency, disciplined ownership, and long-term thinking.

The decisions you make today, quiet, uncelebrated, and intentional, can echo for generations.

And that, to me, is real wealth.

{kind=link}