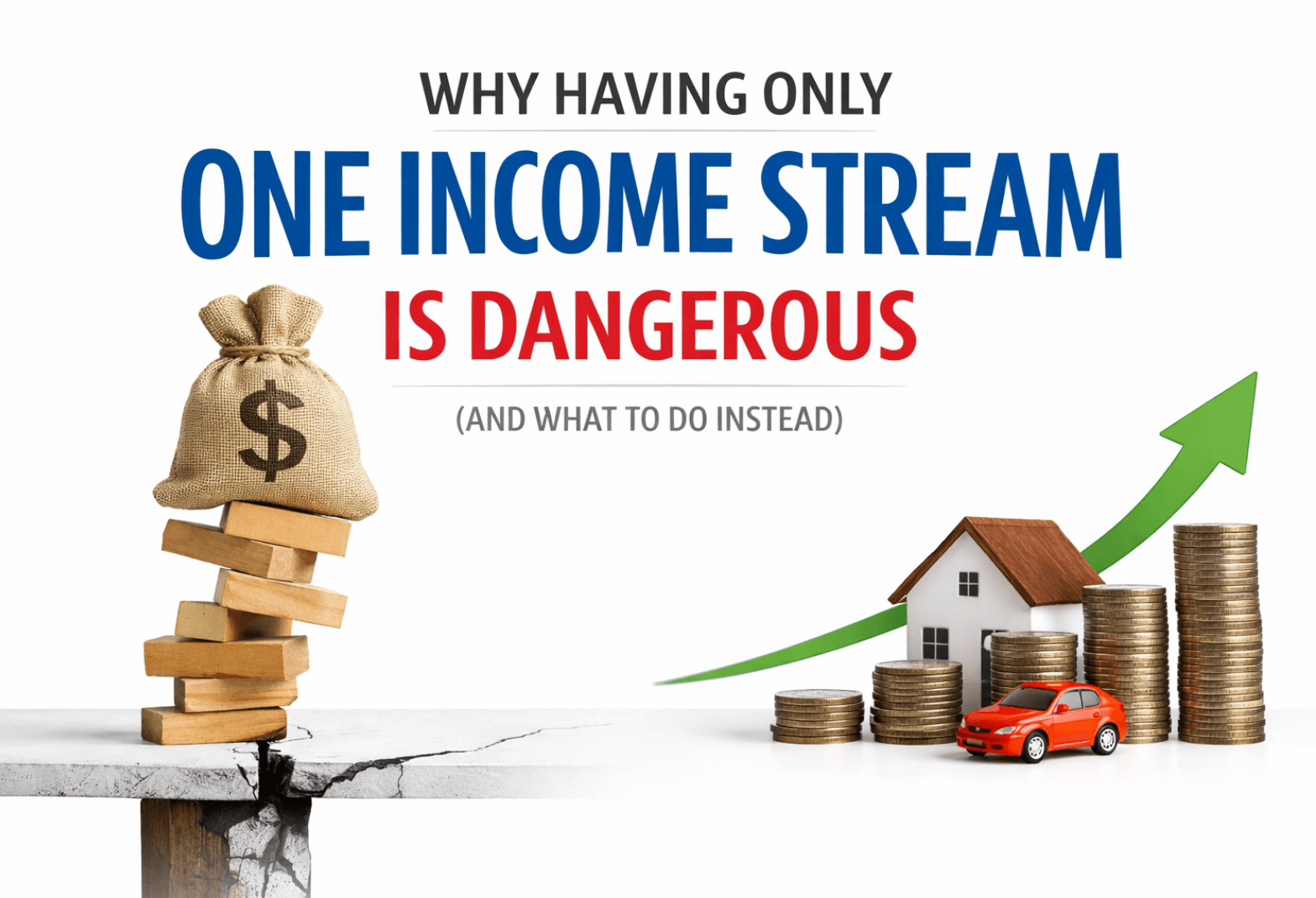

For the majority of my life, I learned that the goal was to have a single, steady income stream.

Get a good job.

Be loyal.

Climb the ladder.

Don’t take unnecessary risks.

If you did that, you were told, everything would work out.

But as I grew older and as I watched economic cycles, layoffs, inflation, pandemics, technological disruption, and silent financial stress ripple through families, I realized something uncomfortable:

One income stream doesn’t equal stability.

It equals dependency.

And being in a dependent position is one of the most dangerous financial positions you can be in.

This article isn’t about hustling for the sake of hustling. It’s not about burning yourself out chasing ten side gigs. And it’s definitely not about shaming people who work traditional jobs.

It’s about risk, how it hides, how it compounds, and how relying on a single source of income quietly puts your future, your family, and your freedom at the mercy of forces you don’t control.

The Illusion of Stability With One Income Stream

Why a Paycheck Feels Safer Than It Really Is

A paycheck feels safe because it’s predictable.

You know when it’s coming.

You know roughly how much it will be.

You build your entire life around that certainty.

But predictability is not the same thing as security.

A paycheck depends on:

- Your employer is staying profitable

- Your role remains relevant

- Your health is holding up

- The economy is not turning against you

- Someone else deciding you’re still worth paying

There are many variables for something that most people consider “stable.”

The danger isn’t that a paycheck is harmful. The danger is believing it’s guaranteed.

How Modern Economies Punish Single-Source Earners

In older economic systems, loyalty was rewarded. Careers lasted decades. Skills aged slowly.

That world no longer exists.

Today:

- Companies restructure overnight

- Entire industries get disrupted

- Automation and AI replace roles faster than people can retrain

- Inflation eats purchasing power silently

Relying on a single source of income exposes you to the full impact of every external shock.

There’s no buffer. No backup. There is no secondary engine to keep things moving.

Predictable Income vs Secure Income

Predictable income answers the question:

“How much will I earn this month?”

Secure income answers a different question:

“What happens if this stops?”

If your financial system collapses the moment your primary income disappears, you don’t have security. You have fragility.

What Happens When That One Income Stream Disappears

Most people avoid planning for income loss because it feels negative or unlikely.

Until it happens.

Job Loss, Layoffs, and Corporate Reality

Layoffs are usually impersonal, but they’re always personal in impact.

It doesn’t matter how loyal you were.

How long did you stay?

How hard you worked.

If the numbers don’t work, you’re gone.

And when your entire financial life depends on that one stream, the damage is immediate:

- Savings drain quickly

- Debt increases

- Stress skyrockets

- Decisions become reactive instead of strategic

Health Issues and Life Events

This is the risk people rarely price in.

If your ability to earn is tied to your ability to show up physically or mentally every day, your health is an unspoken single point of failure.

An injury.

Burnout.

A family emergency.

One income stream leaves no margin for being human.

Economic Shocks You Can’t Control

Recessions don’t ask permission.

Inflation doesn’t wait for raises.

Technology doesn’t slow down, so you can catch up.

When income is diversified, shocks are absorbed.

When income is singular, shocks are devastating.

Why the Middle Class Is Most Exposed to Income Risk

Ironically, the group that perceives the most stability is frequently the most vulnerable.

Fixed Expenses vs Fragile Income

Middle-class lifestyles tend to come with:

- Mortgages

- Car payments

- Insurance

- Subscriptions

- Lifestyle commitments

These expenses are fixed. Your income is not.

When income drops, expenses don’t.

That mismatch is where financial stress lives.

Lifestyle Inflation Creates Silent Dependency

Raises feel like progress, but often they just increase dependency.

Increased income leads to increased spending, higher obligations, and less flexibility.

At a certain point, you’re not working for growth, you’re working to maintain.

Why “Good Jobs” Can Delay Wealth

A good job can:

- Reduce urgency

- Delay ownership

- Create comfort that suppresses long-term thinking

It’s not that jobs are bad.

It’s that jobs alone don’t build resilience or generational wealth.

How the Wealthy Think About Income Differently

Wealthy individuals and families don’t rely on income the way most people do.

They think in systems.

Income Streams vs Income Control

The wealthy ask:

- Who controls this income?

- Can it survive without my daily effort?

- Does it scale?

- Can it be replaced if needed?

They don’t aim for one strong stream.

They aim for multiple controllable streams.

Why the Rich Never Depend on One Source

Even when wealthy people earn a lot from one source, they quietly build others.

Why?

This is due to the risk associated with concentration.

Diversification isn’t about greed, it’s about survival at scale.

Risk Distribution as a Core Strategy

Multiple income streams spread risk across:

- Industries

- Skill sets

- Asset classes

- Time

When one slows down, others keep going.

The Psychological Trap of One Income Stream

The danger isn’t only financial. It’s mental.

Fear-Based Decision Making

When you rely on one income:

- You tolerate bad environments

- You avoid necessary risks

- You stay quiet instead of negotiating

- You trade long-term growth for short-term safety

Fear becomes the decision-maker.

Limited Leverage and Negotiation Power

Leverage comes from options.

If you have one income stream, you have no leverage.

If you have multiple, you gain:

- Confidence

- Negotiation power

- The ability to walk away

Dependency Kills Long-Term Vision

When survival is the priority, strategy disappears.

One income stream keeps you focused on the next paycheck instead of the next decade.

The Compounding Risk Over Time

Time doesn’t reduce income risk. It magnifies it.

Inflation and Erosion

If your income grows more slowly than inflation, you’re moving backward, even if your salary increases.

Multiple streams create more chances to outpace inflation.

Career Ceilings and Plateaus

Every career has limits:

- Salary bands

- Promotion bottlenecks

- Age bias

Relying on one career path assumes it will always keep pace.

That’s a dangerous assumption.

The 30-Year Question

Ask yourself:

If nothing changes, where does this income put me in 30 years?

The answer should not be where you hope, but rather where the math indicates.

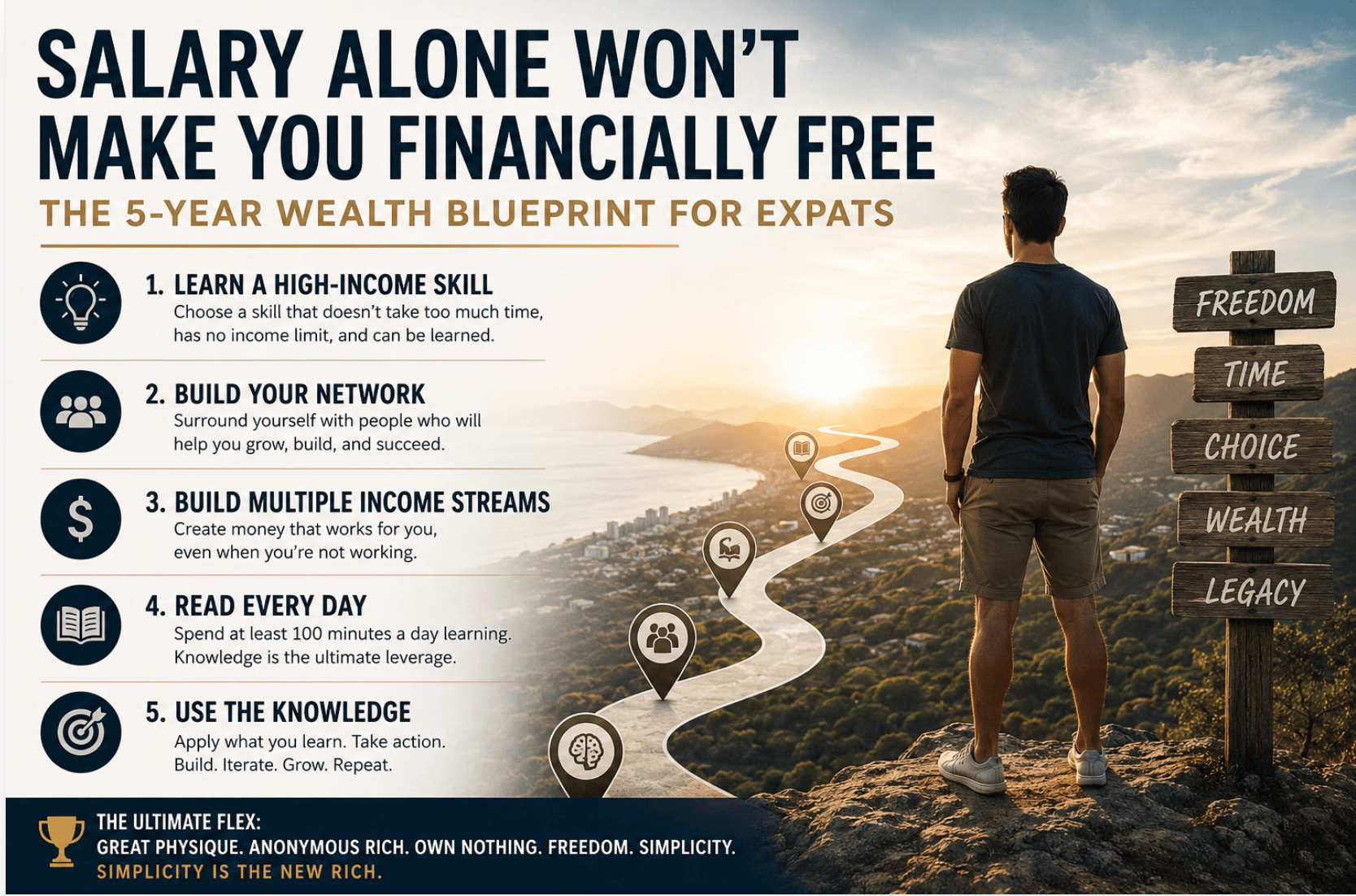

Why Multiple Income Streams Create Financial Resilience

This is where the narrative often gets misunderstood.

Multiple income streams are not about doing everything.

They’re about depending on more than one thing.

Redundancy Is Protection

In engineering, redundancy prevents failure.

In finance, it does the same.

One stream failing shouldn’t collapse your entire system.

Diversification vs Overcomplication

You don’t need ten streams.

You need:

- One primary

- One secondary

- One scalable or asset-based

That alone dramatically reduces risk.

Small Streams, Big Impact

Even small income streams:

- Reduce pressure

- Extend runway

- Improve decision quality

They buy time, and time buys freedom.

Types of Income Streams (From Active to Passive)

Not all income is created equal.

Earned Income

Jobs, freelancing, consulting.

Active. Linear. Time-bound.

These jobs can be useful, but they can also be fragile on their own.

Business Income

Income tied to systems, teams, or products.

More control. More leverage.

Investment Income

Dividends, interest, and capital gains.

Investment income involves the use of capital rather than time.

Asset-Based Income

This includes content, intellectual property, and digital platforms.

Scalable. Often underestimated.

The goal isn’t to jump straight to passive income.

The goal is progression.

Common Myths About Multiple Income Streams

“You Need to Be Rich First”

False.

You need structure, patience, and discipline, not wealth.

“It Takes Too Much Time”

It takes time to build, but it saves time later.

Dependency is far more expensive in the long term.

“It’s Riskier Than One Stable Job”

Concentration is a risk.

Diversification is defense.

How to Start Building a Second Income Stream (Step-by-Step)

This doesn’t require quitting your job tomorrow.

Step 1: Secure Your Primary Income

Stability first.

You build from solid ground, not panic.

Step 2: Build a Skill or Asset

Focus on:

- Skills with leverage

- Assets that compound

- Systems that scale

Step 3: Reinvest Before Lifestyle Upgrades

This is critical.

Reinvesting early income streams accelerates growth exponentially.

Step 4: Stack, Don’t Replace

Don’t abandon income streams too early.

Stack them until the dependency disappears.

When One Income Stream Might Be Temporarily Acceptable

There are exceptions, but only with intention.

Early Career Phases

Learning and skill acquisition matter.

But this phase should have a clear transition plan.

Strategic Focus Periods

Sometimes focus beats diversification, temporarily.

Temporary Must Have an Exit

One income stream without an exit strategy is complacency.

The Long-Term Cost of Doing Nothing

The biggest risk isn’t failure.

It’s stagnation.

Opportunity Cost Over a Lifetime

Years spent dependent are not compounding.

Generational Impact

Your income structure affects:

- Your children’s options

- Your family’s resilience

- Your legacy

Why Your Family Pays the Price

When income collapses, families absorb the shock.

Multiple income streams protect more than just you.

FAQ: Why It Is Dangerous to Have One Income Stream

Could having only one income stream be considered risky?

Yes. Having only one income stream creates a single point of failure in your financial life. If that income stops due to layoffs, health issues, economic downturns, or industry disruption, your entire financial system is immediately at risk. Multiple income streams reduce dependency and increase financial resilience.

Is one income stream ever enough?

One income stream may be temporarily sufficient during early career stages or focused growth periods, but it is rarely enough for long-term financial security or generational wealth.

Over time, inflation, income plateaus, and unexpected life events make reliance on a single income increasingly risky.

How many income streams should I have?

There is no perfect number, but most financially resilient individuals aim for at least two to three income streams.

This often includes one primary earned income, one secondary income, and one scalable or asset-based income. The goal is not quantity—it’s reduced dependency.

What is the safest second income stream to start with?

The safest second income stream is one that:

- Uses an existing skill or knowledge base

- Requires low upfront capital

- Can be built alongside your primary income

Examples include consulting, freelancing, digital products, content-based businesses, or small online ventures. Safety comes from control and sustainability, not speed.

Does having multiple income streams mean working more hours?

Not necessarily. While building additional income streams may require extra effort initially, the long-term goal is to create systems and assets that reduce dependency on time-based work. Over time, diversified income can actually reduce stress and improve work-life balance.

Are multiple income streams riskier than a stable job?

No. Relying on a single income source is often riskier because all financial risk is concentrated in one place. Multiple income streams distribute risk across different sources, industries, and timelines, making your overall financial position more stable.

Can passive income replace a job?

Passive income can eventually replace earned income, but it usually takes time, reinvestment, and patience. Most passive income streams start as active efforts before becoming semi-passive or scalable. The focus should be progression, not immediate replacement.

When should I start building a second income stream?

The best time to start is while your primary income is still stable. Building additional income from a position of stability allows you to make strategic decisions rather than reactive ones. Waiting until your income is under threat often results in hasty and unstable decisions.

What’s the biggest mistake people make with income diversification?

The biggest mistake is chasing too many income streams at once without focus or strategy. Diversification should be intentional, gradual, and aligned with long-term goals, not driven by fear or short-term hype.

How does having multiple income streams support generational wealth?

Multiple income streams create stability, optionality, and compounding advantages over time. They reduce financial shocks, preserve capital, and create assets that can outlast individual careers—key components of building and sustaining generational wealth.

Final Thoughts: One Income Stream Is a Single Point of Failure

Wealth isn’t built on hope.

It’s built on optionality.

Freedom Comes From Options

Options come from diversified income.

The Goal Is Not Busyness

The goal is resilience, control, and time.

Income Diversity Is Responsibility

Not greed.

Not obsession.

Responsibility to yourself and those who depend on you.

If you have one income stream, you’re not behind.

But you are exposed.

And the earlier you reduce that exposure, the more control you reclaim over your future.

{kind=link}