Prosperity isn’t built in moments of excitement.

It’s built quietly, slowly, and almost invisibly.

Most people think wealth comes from big wins, the right investment, the perfect business idea, or the lucky break. In reality, prosperity is far more boring than that. It’s the result of habits repeated over long periods, often when no one is watching and nothing feels urgent.

I’ve learned this the hard way.

I’ve made good money and lost money. I’ve had seasons of discipline and seasons where I ignored the basics. And every time I zoom out and look at what actually moved my financial life forward, it always comes back to the same thing: habits.

Not intelligence.

Not income level.

Not timing.

Habits.

In this article, I’m going to walk you through 10 money habits that increase prosperity over time, not overnight, not next month, but steadily and predictably. These are the habits that compound quietly in the background while most people are chasing shortcuts.

If you adopt even a few of these and stick with them long enough, your financial life will look very different a decade from now.

Why Prosperity Is Built Through Habits, Not Windfalls

There’s a reason lottery winners and professional athletes often end up broke. It’s not because they didn’t earn enough money. It’s because money amplifies habits. It doesn’t replace them.

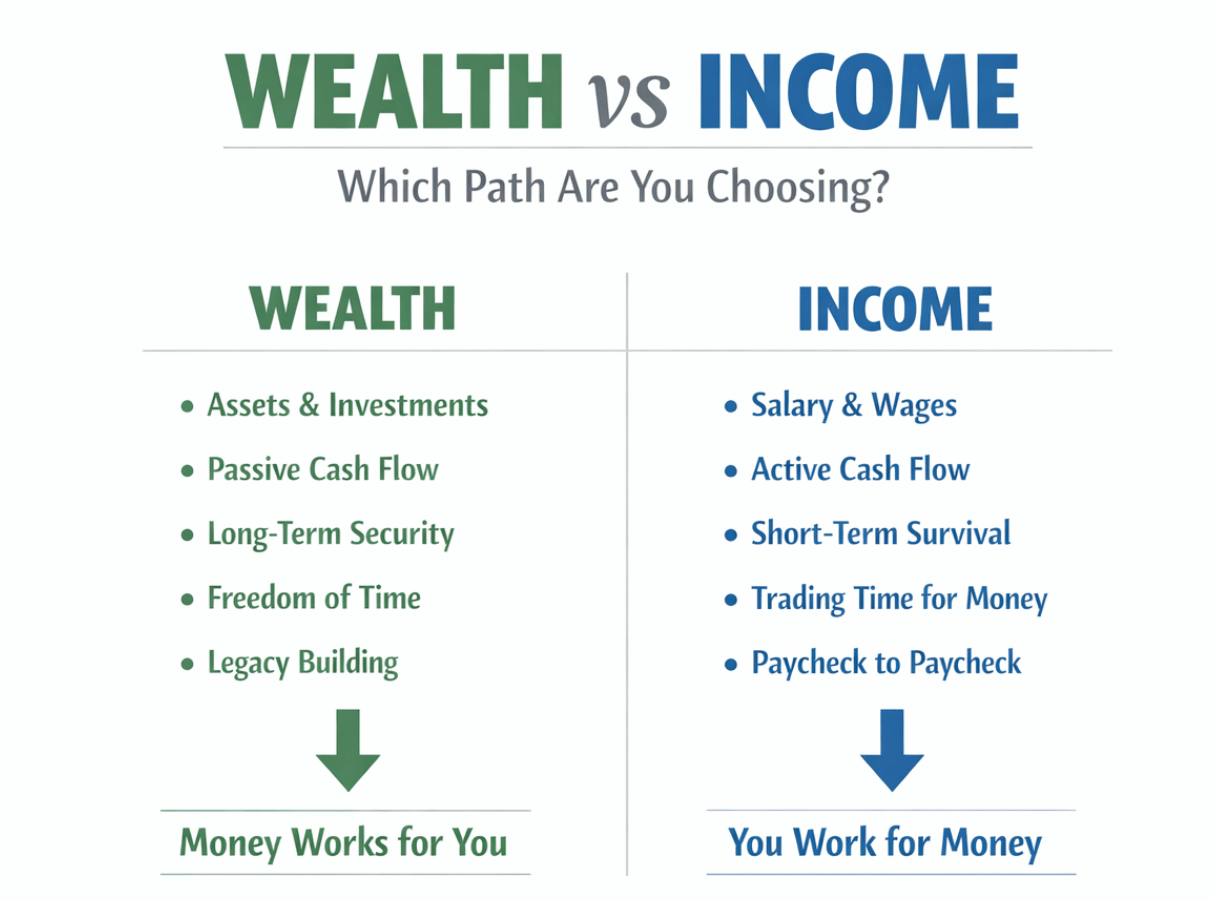

Prosperity is not about how much money passes through your hands. It’s about what stays, what grows, and what compounds.

The Difference Between Getting Rich and Staying Prosperous

Getting rich can happen quickly. Staying prosperous takes discipline.

Anyone can have a good year. Prosperity shows up when you can have a bad year, or a bad decade, and still be financially stable, flexible, and calm.

Habits create that stability. Windfalls don’t.

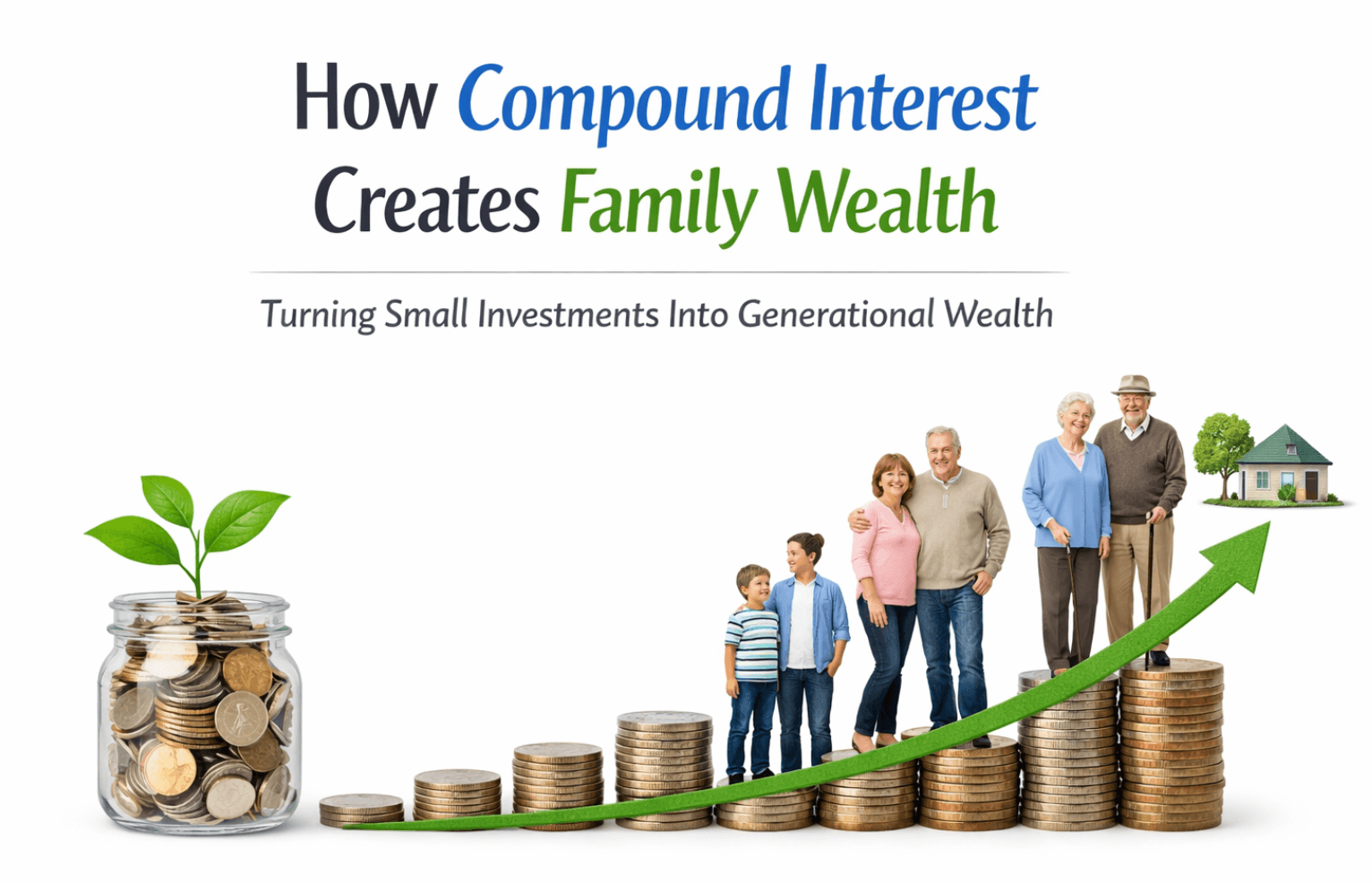

Why Small Financial Decisions Compound Over Decades

A decision that feels insignificant today can quietly shape your financial future.

- Saving a small percentage consistently

- Avoiding one unnecessary lifestyle upgrade

- Reinvesting profits instead of spending them

Individually, these decisions feel almost meaningless. Over 20 or 30 years, they are the difference between stress and freedom.

The Role of Time, Behavior, and Consistency

Time is the multiplier most people ignore.

Everyone wants fast results, but prosperity doesn’t respond to urgency. It responds to consistency. The people who win financially are rarely the most aggressive. They’re the most patient.

Habit #1: Spend Less Than You Earn (Always)

This sounds obvious, but it’s where everything begins and where most people fail.

You cannot out-earn bad spending habits.

No investment strategy, side hustle, or income increase can compensate for consistently spending more than you make.

Why This Is the Non-Negotiable Rule of Prosperity

Every dollar you don’t spend has three possible futures:

- It can become a security

- It can become an investment

- It can become freedom

Every dollar you overspend steals one of those futures.

Prosperity requires margin. Without margin, every unexpected expense becomes a crisis.

The Hidden Cost of Lifestyle Inflation

Lifestyle inflation is the silent killer of wealth.

As income rises, spending increases more quickly. nicer cars, better apartments, more subscriptions, more “rewards.” None of it feels reckless. All of it feels deserved.

Until years pass and nothing has changed financially.

How to Automate This Habit Without Willpower

Willpower is unreliable. Systems aren’t.

- Set savings and investments to happen automatically

- Base your lifestyle on your previous income, not your current one

- Increase savings when income increases, not spending

When spending less than you earn becomes automatic, prosperity stops being fragile.

Habit #2: Pay Yourself First

Most people try to save what’s left at the end of the month. That rarely works because there’s usually nothing left.

Paying yourself first flips the equation.

What “Paying Yourself First” Really Means

It means your future matters more than your present impulses.

You decide in advance how much of your income is non-negotiable for saving or investing, and you live on the rest.

Why Saving After Expenses Never Works

Expenses expand to match available money. Always.

If you wait to see what’s left, you’re relying on restraint in a system designed to eliminate it.

Simple Systems to Make This Automatic

- Automatic transfers on payday

- Separate accounts for spending and saving

- Investment contributions scheduled in advance

Once this habit is in place, prosperity stops being optional.

Habit #3: Treat Saving as a Fixed Expense

Saving isn’t something you try to do. It’s something you owe yourself.

Just like rent or utilities.

Why Savings Should Be Non-Optional

Savings buy time. Time buys options.

Without savings, every decision becomes reactive. With savings, you can think strategically.

Emergency Funds vs. Wealth-Building Capital

Prosperous people separate safety from growth.

- Emergency funds protect you

- Investments grow you

Mixing the two creates anxiety and bad decisions.

How Much to Save at Different Income Levels

The exact percentage matters less than consistency.

Start small if you must. Increase slowly. The habit matters more than the number.

Habit #4: Invest Consistently, Not Emotionally

Markets reward patience and punish emotion.

Most people do the opposite.

Why Consistency Beats Timing the Market

Waiting for the “perfect moment” usually means waiting forever.

Consistent investing spreads risk over time and removes ego from the equation.

The Long-Term Power of Dollar-Cost Averaging

When you invest regularly:

- You buy high

- You buy low

- You avoid catastrophic mistakes

It’s boring, and that’s why it works.

Common Emotional Traps That Kill Prosperity

- Panic selling

- Chasing hype

- Abandoning long-term plans for short-term fear

Prosperity requires emotional discipline more than financial intelligence.

Habit #5: Avoid Consumer Debt Like a Tax on Your Future

High-interest consumer debt works against compounding.

Every dollar paying interest is a dollar not building wealth.

How High-Interest Debt Destroys Compounding

Debt grows predictably, against you.

Prosperity requires that compounding works in your favor, not the bank’s.

Good Debt vs. Bad Debt Explained Simply

Good debt tends to:

- Produce income

- Increase productive capacity

Bad debt tends to:

- Fund consumption

- Depreciate

Knowing the difference changes everything.

A Step-by-Step Plan to Eliminate Consumer Debt

- Stop adding new debt

- Focus on the highest interest first

- Redirect freed cash into assets

Debt freedom isn’t glamorous. It’s powerful.

Habit #6: Increase Income Without Increasing Lifestyle

Income growth is only powerful if you capture it.

Otherwise, it just funds a more expensive version of the same life.

Why Income Growth Alone Doesn’t Create Prosperity

Many high earners live paycheck to paycheck.

Income creates opportunity. Habits determine results.

How to Capture Raises, Bonuses, and Side Income

Decide in advance where extra income goes:

- Investments

- Debt reduction

- Business capital

Not lifestyle upgrades.

Turning Income Growth Into Long-Term Wealth

The gap between what you earn and what you live on is where prosperity lives.

Habit #7: Reinvest Profits Instead of Spending Them

This habit separates wealthy builders from high-income consumers.

The Difference Between Income and Wealth

Income feeds today. Wealth feeds tomorrow.

Spending profits feels rewarding. Reinvesting them is transformative.

Why Reinvestment Accelerates Prosperity

Reinvestment compounds:

- Skills

- Assets

- Opportunities

It shortens the distance between where you are and where you want to be.

Real Examples of Reinvestment Compounding Over Time

Businesses grow. Portfolios scale. Income streams multiply.

Not because of luck, but because profits were treated as seeds, not rewards.

Habit #8: Track Net Worth, Not Just Income

Income tells you how fast money comes in.

Net worth tells you whether you’re winning.

Why Net Worth Is the True Scorecard

Prosperity is measured by what you keep and grow, not what you earn.

Tracking net worth forces honesty.

Assets vs. Liabilities Explained Clearly

Assets put money in your pocket.

Liabilities take money out.

The direction of your net worth tells the real story.

How Often You Should Track Net Worth (and Why)

Quarterly is enough.

The goal isn’t obsession. It’s awareness.

Habit #9: Build Assets That Produce Income

Prosperity accelerates when income is no longer tied entirely to your time.

What Income-Producing Assets Really Are

- Businesses

- Investments

- Intellectual property

Anything that continues to generate cash flow without constant effort.

Active vs. Passive Income Assets

Most assets start active and become passive over time.

The key is building systems, not chasing myths.

Starting Small and Scaling Over Time

No one starts with a massive portfolio.

They start with one asset and patience.

Habit #10: Think in Decades, Not Months

This habit changes everything.

Why Short-Term Thinking Sabotages Prosperity

Short-term thinking leads to:

- Impulsive decisions

- Emotional reactions

- Constant course-changing

Prosperity requires direction, not speed.

How Long-Term Thinking Changes Financial Decisions

You stop asking:

“What’s the fastest win?”

And start asking:

“What will still matter in 20 years?”

Aligning Daily Habits With Long-Term Wealth Goals

Daily actions compound into decades of results.

That’s the real game.

Common Money Habits That Quietly Destroy Prosperity

Some habits don’t feel dangerous until time exposes them.

Chasing Returns Instead of Building Foundations

High returns without stability lead to collapse.

Foundations matter more than performance.

Lifestyle Inflation Disguised as “Success”

Looking wealthy is not the same as being prosperous.

Often, it’s the opposite.

Over-Leverage and Financial Fragility

Leverage magnifies mistakes.

Prosperous people prioritize resilience.

How to Implement These 10 Money Habits Starting Today

You don’t need perfection. You need momentum.

A Simple 30-Day Habit Implementation Plan

- Week 1: Track spending and net worth

- Week 2: Automate saving and investing

- Week 3: Eliminate one bad habit

- Week 4: Lock in systems

Which Habit to Start With Based on Your Situation

- Low savings → Pay yourself first

- High debt → Eliminate consumer debt

- High income, low progress → Capture lifestyle inflation

How to Stay Consistent When Motivation Fades

Systems beat motivation.

Always.

FAQ: 10 Money Habits That Increase Prosperity Over Time

What are the most important money habits for long-term prosperity?

The most important money habits for long-term prosperity are spending less than you earn, paying yourself first, avoiding consumer debt, investing consistently, and thinking long-term.

These habits create margin, allow compounding to work in your favor, and reduce financial stress over time. Prosperity is built through consistency, not quick wins.

Can small money habits really increase prosperity over time?

Yes. Small money habits compound over time in powerful ways. Saving or investing even a small percentage consistently, avoiding lifestyle inflation, and reinvesting profits can lead to significant wealth over decades. Time magnifies behavior, which is why habits matter more than income level.

How long does it take for money habits to show results?

Some benefits, like reduced stress and better cash flow, can appear within months. True financial prosperity, however, typically shows meaningful results over years or decades. Money habits work slowly at first and then accelerate as compounding takes effect.

Is it better to focus on saving or investing first?

Both matter, but saving usually comes first. Building an emergency fund creates stability and prevents debt, while investing builds long-term wealth. Prosperous individuals separate safety (savings) from growth (investments) and fund both consistently.

What money habits keep people from becoming prosperous?

Common habits that prevent prosperity include lifestyle inflation, relying on credit for consumption, chasing high returns instead of building foundations, emotional investing, and failing to track net worth. These behaviors quietly undermine long-term wealth, even with a high income.

How much should I save each month to build prosperity?

There is no single perfect number. A good starting point is saving at least 10–20% of income, but consistency matters more than percentage.

As income grows, increasing savings and investments without increasing lifestyle accelerates prosperity significantly.

Why is avoiding consumer debt so important for wealth building?

High-interest consumer debt works against compounding by draining future income. Interest payments reduce cash flow, limit investment ability, and increase financial stress. Avoiding consumer debt allows money to compound in your favor rather than against you.

What’s the difference between income and prosperity?

Income is how much money you earn. Prosperity is how financially secure, flexible, and resilient you are over time.

Someone with a high income but no savings or assets may not be prosperous, while someone with a moderate income and strong habits often is.

How does tracking net worth help increase prosperity?

Tracking net worth provides a clear picture of financial progress by showing the relationship between assets and liabilities. It shifts focus from earning more money to building real wealth and encourages better long-term decision-making.

Can these money habits help even if I don’t earn much?

Yes. Money habits matter at every income level. While higher income can accelerate results, poor habits can destroy wealth just as quickly.

Many people build prosperity on modest incomes by controlling spending, avoiding debt, and investing consistently.

What is the fastest way to improve my financial situation using habits?

The fastest improvement usually comes from eliminating high-interest debt, controlling spending, and automating savings.

These changes immediately improve cash flow and reduce financial pressure, creating momentum for long-term prosperity.

Are money habits more important than financial knowledge?

In most cases, yes. Many people understand what they should do, but fail to act consistently. Prosperity depends more on behavior and discipline than on complex financial strategies. Simple habits executed over time outperform advanced tactics used inconsistently.

How do I stay consistent with money habits when motivation fades?

Consistency comes from systems, not motivation. Automating savings, investing, and bill payments removes emotion and decision fatigue. Prosperous people design systems that make good habits the default.

Final Thoughts: Prosperity Is Boring, Predictable, and Powerful

Prosperity doesn’t come from dramatic moments.

It comes from doing the right things long after the excitement wears off.

The habits in this article won’t impress anyone on social media. They won’t make you feel rich tomorrow. But over time, they quietly create something far more valuable:

Stability.

Freedom.

Control.

And that’s what real prosperity looks like.

{kind=link}